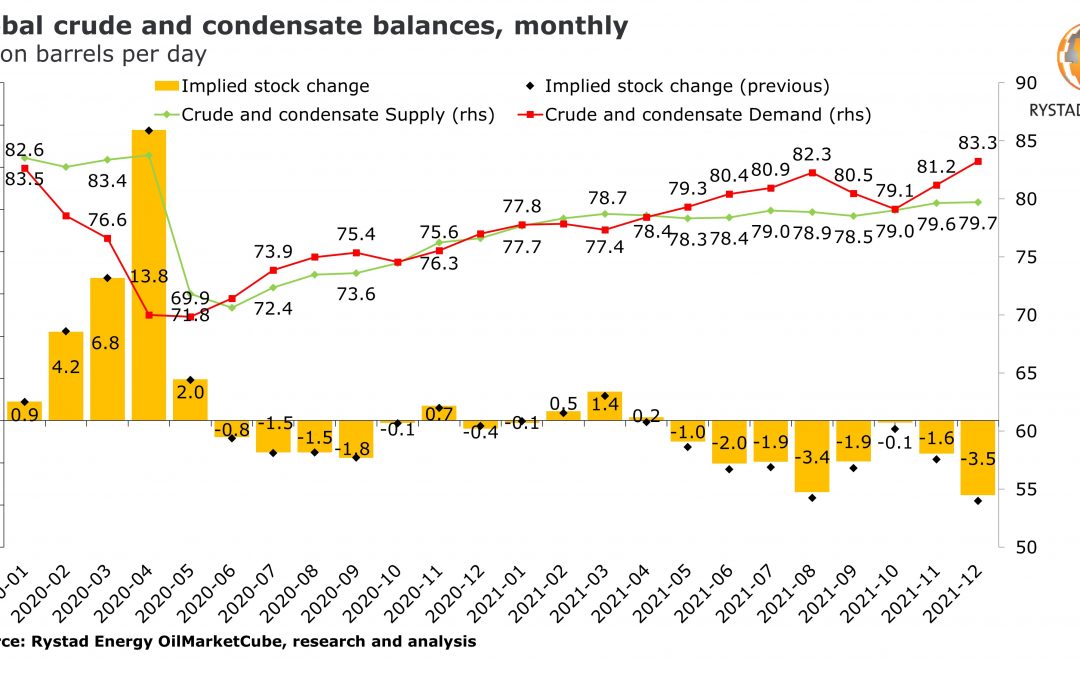

The Covid-19 pandemic has devastated crude and condensate demand in 2021, creating massive supply surpluses and filling up inventories, causing producers to slash output in order to keep prices at somewhat profitable levels. Rystad Energy’s latest balances, however, show that 2021 could offer producers a window of opportunity, as monthly supply deficits may reach their highest level in years.

Although crude and condensate supply will still exceed demand in the first quarter of 2021, Rystad Energy expects that vaccination campaigns will help bring a rapid recovery going forward. Monthly supply deficits will start from May, reaching a high of around 3.4 million barrels per day in August. As deficits continue uninterrupted through the year, August’s high could be repeated, if not exceeded by year-end.

Entering 2021, Rystad Energy expects a largely balanced oil market in January, with supply and demand hovering between 77.7 and 77.8 million bpd. The effect of global lockdowns will be felt even more in February and March as demand will not follow the growing supply and stay capped at 77.9 million bpd and 77.4 million bpd respectively, creating a surplus of 0.5 million bpd in February and 1.4 million bpd in March. A minor surplus will also be recorded in April but the market will recover shortly after.

It is important to highlight that our current supply base case assumes the terms of the latest OPEC+ agreement stay unchanged and the group’s production remains flat after January. We also assume stellar compliance within OPEC+ going forward, as well as limited upside to US supply and Iranian barrels coming back only in 2022. However, with the balances entering a period of acute deficit already in the second quarter of 2021, an upward revision to supply might be around the corner.

“Our monitors in the US are starting to point at stronger activity. As we have warned our clients before, shale is a monster than you can slowdown, but cannot kill. In addition, there are winds of change forecasted in the geopolitical realm next year,“ says Bjornar Tonhaugen, Head of Oil Markets at Rystad Energy.

A change of administration in the US could mean that Iran comes back faster than we anticipate in our current base case, either because Biden’s team decides to remove sanctions altogether or because countries like China or India feel confident enough that the new administration will turn a blind eye to the existing sanctions and ramp up imports from the Persian nation.

There is always room for deviation from projections, especially in such a volatile environment as policies can change. The coming deficits will create extra room for OPEC+ to hike production from May-21 versus our base case, which in turn can affect monthly balances. OPEC+ output, as usual, will have to fight for market share with US shale, which is currently turning a corner with increased activity.

Source: Hellenic Shipping