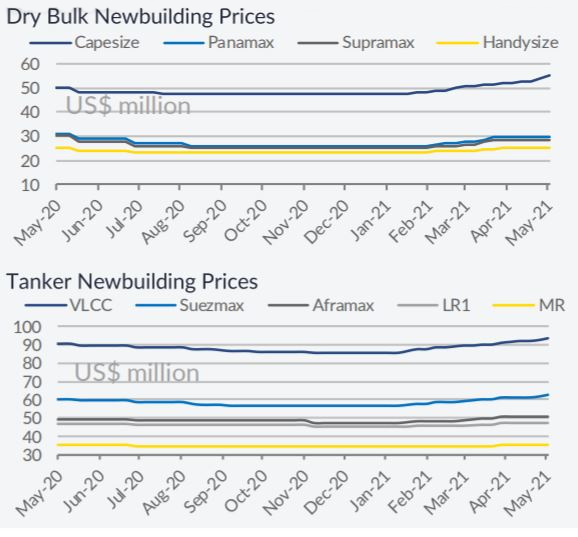

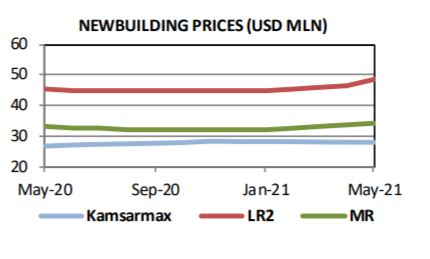

Activity has continued to be more than healthy, in both the newbuilding and S&P markets over the course of the past week. In its latest weekly report, shipbroker Allied Shipbroking said that “things continue to look encouraging on the newbuilding market front, with a fair number of transactions emerging again this past week. The recent trend noted in terms of activity, has given a fair boost on the pricing front as well, with a fair increase in all prices having already been observed since the start of 2021. In part this has also helped shipbuilders absorb some of the extra construction cost that has accumulated from the rapid increases being noted in steel plate prices over the past few months. In terms of dry bulkers, we continue to see activity emerge though at a slower pace and with the main focus having shifted considerably towards Kamsarmax designs.

On the side of tanker, things seem to have slowed down considerably, something that has been more or less expected given the state of the market in terms of earnings right now. The big ticket item this week has been Gas carriers, with a fresh flurry of activity having come to light and a major focus on the LPG front. This, along with keen interest on the container front, are likely to feed a fair portion of the market over the coming weeks, with both these markets showing very promising indications, both in terms of sentiment and current earnings performance”, Allied said.

In a separate note, Banchero Costa added that ‘the container Newbuilding market remained the centre of the action: HMM placed orders for 12 x 13.248 teu at Daewoo and Hyundai. All vessels will be conventional fuel and Neo Panamax type. Prices usd 120 Mio per unit. Deliveries will start as from end 2024 till September 2025.

Another major Owner Zodiac Maritime exercised option for 4 x 15.500 teu at Daewoo at prices of usd 108.3 Mio per unit for delivery as from 04/2024 till 04/2025. The other driving force this week was in the gas sector. NYK Japan added four 170.520 cum. LNG carriers to the Samsung orderbook with deliveries starting from January 2024. The quartet, ordered at unknown levels, is stemmed for charter to Total and will serve the Mozambique project”.

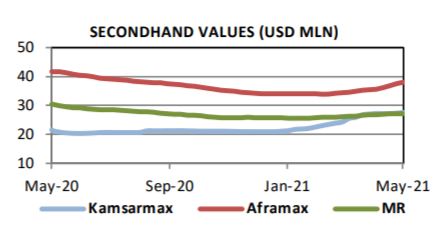

Meanwhile, in the S&P market this past week, Banchero Costa said that “in the dry market, a 10 years old Capesize has been sold through online auction in China Tiger Shandong abt 180k blt 2011 Qingdao Beihai at USD 23.31 to c.of Richland. In the past months same owners has sold Tiger Liaoning abt 180k blt 2011 Qingdao Beihai at USD 21.01 Mill. Greek Container Owners Costamare is rumoured to be behind purchase of kamsarmaxes, Spring Aeolian (abt 83k blt 2012 Sanoyas SS/DD 1/22 BWTS fitted) at usd 21.3 and Pedhoulas Builder and Pedhoulas Farmes abt 82k blt 2012 Zhejiang at USD 44.5 Mill. Furthermore a Tier II kamsarmax Countess I abt 80k blt 2013 Jiangsu has been sold at USD 18.8 Mill, one month ago Wanisa abt 79k blt 2012 Jiangsu has been sold at USD 15 Mill. to Chinese buyers Japanese controlled supramaxes Pacific Hero abt 58k blt 2012 Kawasaki and Indigo Traveller abt 56k blt 2011 Mitsui were sold at USD 18 Mill and 15.8 Mill. respectively. Two weeks ago Lowlands Patrasche abt 58k blt 2013 Tsuneishi has been reported at USD 18.2 Mill.

Two Chinese controlled supramaxes Great Legend + Great Praise abt 52k blt 2006 Tsuneishi Cebu are committed in the mid/high 11’s each to Chinese buyers on a waiving inspection basis. During the week it was registered a strong appetite for handy bcs pushed by a strong chartering market. Ultra Calbuco abt 38k blt 2017 Imabari and Ultra Osorno abt 38k blt 2018 Shimanami sold usd 45m enbloc to Pacific Basin, while Nordrubicon and Nordcolorado abt 38k blt 2016 Ouhua were done respectively at USD 18.28 mill and USD 18.045 mill. A Japanese controlled Basic Rainbow abt 38k blt 2011 Imabari has been committed in excess of USD 14.6 Mill, understand 10 Buyers (from China and Greece) has registered interest in the vessel. In the tanker market, three LR2s Nissos Schinoussa + Nissos Therassia + Nissos Heraclea abt 114,300 dwt built 2015 Hyundai Heavy, Korea (BWTS-Fitted ss/dd passed) were reported sold to Torm for USD 40 mil each”, the shipbroker concluded.

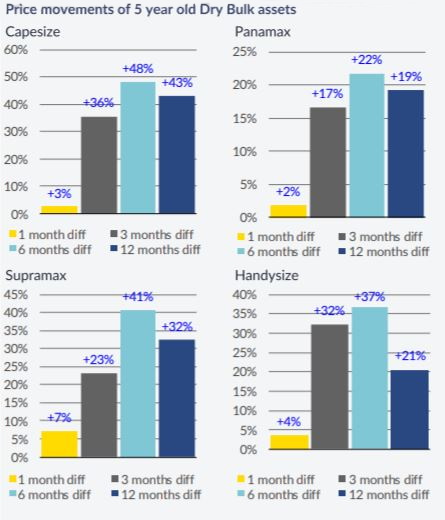

Allied Shipbroking added that “on the dry bulk side, the bullish momentum in terms of activity noted seems rather abundant for the time being. For yet another week, the volume of transactions taking place was relatively strong, despite somehow the slight correction noted on the side of earnings as of late. Moreover, we notice a seemingly well distributed buying appetite across different asset classes and age groups, which could suggest that this trend can be sustained at this point.

With asset prices being also on an upward path for a fair while now, we can expect a very interesting SnP market to unfold over the coming weeks. On the tanker side, it was another week of very firm activity, which suggests an SnP market that is currently on the rise (both in asset price levels and transaction volumes). During the past week, we saw a plethora of deals taking place, with VLs and Aframaxes taking the lead at this point. Notwithstanding this, given the current state of play from the side of earnings, we can’t take this trend for granted”, Allied concluded.

Source: Hellenic Shipping